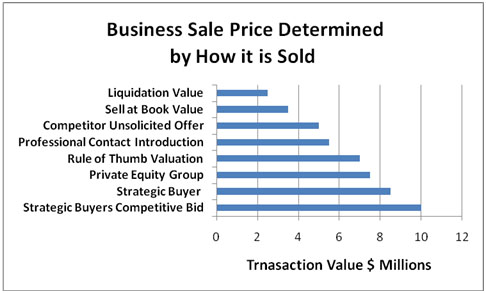

How much is my business worth? That depends. Of course it depends on profits, sales, EBITDA, and other traditional valuation metrics. A surprisingly important factor, however, is how you choose to sell it. If your business is larger, complex, unusual, strategic, with a high component of intellectual property or technology and subject to a broad interpretation of value in the marketplace then how you choose to sell it can result in swings of literally millions of dollars in transaction value. The Graph below attempts to illustrate this concept:

The way to achieve the most value from the sale of your company is to get several strategic buyers all competing in a soft auction process. That is the holy grail of company valuation. There are several exit or value options. Let’s examine each one starting with the lowest which is liquidation value.

Liquidation Value – This is basically the sale of the hard assets of the business as it ceases to be a going concern. No value is given for good will, brand name, customer lists, or company earnings capability. This is a sad way to exit a business that you spent twenty years building. This method of selling often occurs when the owner has a debilitating health issue or dies and his estate is forced to sell.

Book Value – is simply an accounting treatment of the physical assets. Book value is generally not even close to the true value of a business. It only accounts for the depreciated value of physical assets and does not take into account such things as earnings power, proprietary technology, competitive advantage, growth rate, and many other important factors. In case you are working on a shareholder agreement and looking for a methodology for calculating a buy-out, Book value is a terrible metric to use. A better approach would be a multiple of sales or EBITDA. Minority shareholders often unknowingly sign shareholder agreements that provide a book value buyout if the minority shareholder decides to cash out.

Unsolicited Offer to Buy from a Competitor – This is the next step up in value. The best way I can describe the buyer mindset is that they are hoping to get lucky and buy your company for a bargain price. If the unsuspecting seller bites or makes a weak counter offer, the competitor gets a great deal.

How should you handle this situation so you do not have this outcome? We suggest that you do not let an outside force determine your selling timeframe. However, we recognize that everything is for sale at the right price. That is the right starting point. Get the buyer to sign a confidentiality agreement. Provide income statement, balance sheet and your yearly budget and forecast.

How should you handle this situation so you do not have this outcome? We suggest that you do not let an outside force determine your selling timeframe. However, we recognize that everything is for sale at the right price. That is the right starting point. Get the buyer to sign a confidentiality agreement. Provide income statement, balance sheet and your yearly budget and forecast.

Determine the number that you would accept as your purchase price and present that to the buyer. You may put it like this, ” We really were not considering selling our company, but if you want us to consider going through the due diligence process, we will need an offer of $6.5 million. If you are not prepared to give us a LOI at that level, we are not going to entertain further discussions.”

A second approach would be to ask for your number and if they were willing to agree, then you would agree to begin the due diligence process. If they were not, then you were going to engage your merger and acquisition advisor and they would be welcome to participate in the process with the other buyers that were brought into the competitive selling process.

Another tactic from this bargain seeker it to propose a reasonable offer in a qualified letter of intent and then embark on an exhaustive due diligence process. He uncovers every little flaw in the target company and begins the process of chipping away at value and lowering his original purchase offer. He is counting on the seller simply wearing down since the seller has invested so much in the process and accepting the significantly lower offer.

Buyer Introduced by Seller’s Professional Advisors – Unfortunately this is a commonly executed yet flawed approach to maximizing the seller’s transaction value. The seller confides in his banker, financial advisor, accountant, or attorney that he is considering selling. The well-meaning advisor will often “know a client in the same business” and will provide an introduction. This introduction often results in a bidding process of only one buyer. That buyer has no motivation to offer anything but a discounted price.

Valuation From a Professional Valuation Firm – At about the midpoint in the value chain is this view of business value. These valuations are often in response to a need such as gift or estate taxes, setting up an ESOP, a divorce, insurance, or estate planning. These valuations are conservative and are generally done strictly by the numbers. These firms use several techniques, including comps, rules of thumb, and discounted cash flow. These methods are not great in accounting for strategic value factors such as key customers, intellectual capital, or a competitive bidding process from several buyers.

Private Equity or Financial Buyer – In this environment of tight credit, the Private Equity Groups still have a good amount of capital and need to invest in deals. The very large deals are not currently getting done, but the lower middle market transactions are still viable. The PEG’s still have their roots as financial buyers and go strictly by the numbers, and they have tightened the multiples they are willing to pay. Where two years ago they would buy a bricks and mortar company for 6 ½ X EBITDA, they are now paying 5 X EBITDA.

Strategic Buyers in a Bidding Process – The Holy Grail of transaction value for business sellers is to have several buyers that are actively seeking to acquire the target company. One of the luckiest things that has happened in our client’s favor as they were engaged in selling their company was an announcement that a big company just acquired one of the seller’s competitors. All of a sudden our client became a strategic prized target for the competitors of the buying company. If for no other reason than to protect market share, these buyers come out of the woodwork with some very aggressive offers.

This principal holds as an M&A firm attempts to stimulate the same kind of market dynamic. By positioning the seller as a potential strategic target of a competitor, the other industry players often step up with attractive valuations in a defensive posture.

This principal holds as an M&A firm attempts to stimulate the same kind of market dynamic. By positioning the seller as a potential strategic target of a competitor, the other industry players often step up with attractive valuations in a defensive posture.

Another value driver that a good investment banker will employ is to establish a strategic fit between seller and buyer. The advisor will attempt to paint a picture of 1 + 1 = 3 ½. Factors such as eliminating duplication of function, cross selling each other’s products into the other’s install base, using the seller’s product to enhance the competitive position of the buying company’s key products, and extending the life of the buyer’s technology are examples of this artful positioning.

Of course, the merger and acquisition teams of the buyers are conditioned to deflect these approaches. However, they realize that their competitors are getting the same presentation. They have to ask themselves, “Which of these strategic platforms will resonate with their competitors’ decision makers?”

As you can see, the value of your business can be subjectively interpreted depending on the lenses through which it is viewed. The decision you make on how your business is sold will determine how value is interpreted and can result in 20%, 30%, 40%, or even 100% differences in your sale proceeds.

Dave Kauppi is the editor of The Exit Strategist Newsletter and a Merger and Acquisition Advisor and President with MidMarket Capital, Inc. MMC is a private investment banking, merger & acquisition firm specializing in providing corporate finance and intermediary services to entrepreneurs and middle market corporate clients in information technology, software, high tech, and a variety of industries. Dave began his Merger and Acquisition practice after a twenty-year career within the information technology industry. His varied background includes positions in hardware sales, IT Services (IBM’s Service Bureau Corp. and Comdisco Disaster Recovery), Software Sales, computer leasing, datacom, and Internet. The firm counsels clients in the areas of merger and acquisition and divestitures, achieving strategic value, deal structure and terms, competitive negotiations, and “smart equity” capital raises. Dave is a Certified Business Intermediary (CBI), is a registered financial services advisor representative and securities agent with a Series 63 license. Dave graduated with a degree in finance from the Wharton School of Business, University of Pennsylvania. For more information or a free consultation please contact Dave Kauppi at (630) 325-0123, email davekauppi@midmarkcap.com or visit our Web page http://www.midmarkcap.com