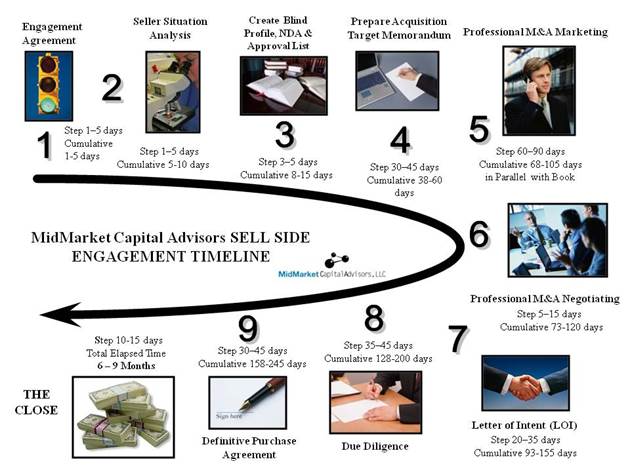

ENGAGEMENT AGREEMENT

The first step is the execution of the Engagement Agreement. It spells out the activities YOUR M&A ADVISOR will perform and details the fee structure. The key elements of the agreement are monthly fees, success fees, cash at close, and cancellation.

SELLER SITUATION ANALYSIS

As Steven Covey would say, “Begin with the end in mind.” It is important that seller and investment banker have a meeting of the minds about the Seller’s desired outcomes. We will discuss valuation expectations, deal structure (i.e. cash at close, seller financing, earn-outs, etc.) seller’s post sale stay-on period and what capacity he/she desires (full time for 3 months followed by 20 hours a week for 6 months, for example).

CREATE NDA (NON-DISCLOSURE AGREEMENT),

BLIND PROFILE AND APPROVAL LIST

We have a philosophy that it is to the seller’s great advantage to get the sales process completed as soon as possible and that is how we operate. Our objective is to have the Blind Profile (a 2 page document that describes the company and the strategic opportunity created through the acquisition without revealing the identity of the seller) completed within the first week. The NDA is a standard document that we customize by adding the client number, i.e. Client # 060524. That number is used with prospective buyers until the NDA’s are executed.

PREPARE ACQUISITION TARGET MEMORANDUM (ATM)

This is an area where our procedure differs from most in our profession. Through experience we have learned that it can be a drawn out period to get all the company information necessary to complete this document to ours and our seller’s satisfaction. Some of the competitors do no marketing of the company before all the I’s are dotted and the T’s are crossed on this document. That could be 4 months! We believe that our client should not be paying a monthly fee to an M&A firm waiting for information. We process in parallel. We immediately produce the blind profile and begin the contact process while we are preparing the ATM. There is no better motivator than 5 executed NDA’s with potential buyers to get the seller to provide the necessary information to complete the document.

PROFESSIONAL M&A MARKETING

Our process is the most effective in compressing the time period between start and closing. It is a direct sales approach that involves phone calls to each of the buyer prospects. It is very labor intensive, requiring on average 10 dials for every successful contact. When we reach the target, we have less than one minute to articulate the opportunity and get their attention.

After all, presidents of companies are very busy men. The importance of our industry specialization is quite evident here because we speak the language. Our credibility is established with this prospect and it increases the likelihood that he will seriously consider the opportunity. If he is interested, we ask for his email (if we don’t already have it) and we email him the combined Profile/NDA. We enter a follow-up task in our contact management system for 3 days if we have not received the executed NDA. If not we are back on the phone with a friendly reminder.

Another differentiator in our process is the management of the process. We keep detailed records of every phone call, email, response, reaction, and buyer feedback. Every week we have a Status Update Meeting with our client and they are provided with the Status Update Report which details where every prospect is in the “sales” process. For example, we track every NDA executed, any prospect feedback, and alter our strategic positioning or approach to improve our future effectiveness.

PROFESSIONAL M & A NEGOTIATING

This is a critical step to have the best representation you can have. Your M&A Advisor earns their fees in this step many times over. The buyer is trying to buy your company on the most favorable terms and conditions. We are trying to move the terms and conditions in your direction. By turning over every stone and professionally presenting the opportunity to a large universe of the most appropriate buyers we can bring several interested buyers to the table. We get feedback from our seller on what aspects of the offers are most favorable to them and attempt to move our best targets to an offer that combines the best features of all the offers. This is a delicate process because if a buyer feels that he is being leveraged, he will simply withdraw from the process.

LETTER OF INTENT (LOI)

We do a great deal of our negotiating before the LOI. Generally, a LOI says that if we do our due diligence and everything checks out exactly as presented thus far, and we find no surprises, we are willing to offer this much on these terms to buy your business. It is essentially a non- binding or qualified letter of intent. The other feature is there will be a lock out period for all other buyers. In other words, in return for us spending our time and resources in the due diligence process, you can not continue to actively market your company to other buyers for a period of 45 days. That is why we negotiate so hard before the LOI, because we are then precluded from improving the T’s and C’s. If the due diligence is not to their liking, they may try to improve their terms and counter offer. If that happens, we have the right to go back to the other interested parties and solicit competing bids. The only way to prevent bad buyer behavior and an attack on transaction value is to have several interested buyers ready to step in. It is our job to convey this to the LOI author.

DUE DILIGENCE

This process really has two purposes for the buyer: 1. to really understand what they are buying and 2. to try to undo all that hard negotiating we did to get the value and terms in the LOI. This process is extremely detailed and exhaustive. The buyer will most likely want to see every customer contract, sales pipeline, all employee agreements, all supplier agreements, product documentation, all accounts receivable, accounts payable, any legal issues, and they may even want to make customer satisfaction phone calls (disguised for a different purpose). If anything was presented prior to due diligence that is found to not be true or accurate, get ready for a purchase price adjustment far greater than the value of the discrepancy or worse, they simply walk away because they have lost trust. The other thing that occurs is they will interpret their findings in the most favorable way for themselves and attempt to hack away at transaction value. Your M&A Advisor is standing guard at that door and will make certain that any reductions are legitimate.

DEFINITIVE PURCHASE AGREEMENT

If you have not sold a business before, you will be amazed at the length of this document and the incredible number of reps and warranties with requirements for accompanying detailed exhibits. Again, it is very important to have an experienced M&A firm by your side that has established their credibility with the buyer. The attorneys will do the legal work, but the business case is the purview of the buyer, his M&A team, the seller and MMC.

THE CLOSE

Well, we made it. Everyone will probably be mentally drained by this time because even if buyer and seller are behaving in a very professional and respectful manner, the process encompasses an incredible number of issues that must be addressed to both parties’ satisfaction. You will need experienced cool heads during this pressure packed process. Sometimes we all sit in a big conference room at the seller’s attorney’s office and walk around the table and sign 20 piles of documents and sometimes we exchange documents via fax with hard copy follow-up via overnight carrier.

Dave Kauppi is the editor of The Exit Strategist Newsletter and a Merger and Acquisition Advisor and President with MidMarket Capital, Inc. MMC is a private investment banking, merger & acquisition firm specializing in providing corporate finance and intermediary services to entrepreneurs and middle market corporate clients in information technology, software, high tech, and a variety of industries. Dave began his Merger and Acquisition practice after a twenty-year career within the information technology industry. His varied background includes positions in hardware sales, IT Services (IBM’s Service Bureau Corp. and Comdisco Disaster Recovery), Software Sales, computer leasing, datacom, and Internet. The firm counsels clients in the areas of merger and acquisition and divestitures, achieving strategic value, deal structure and terms, competitive negotiations, and “smart equity” capital raises. Dave is a Certified Business Intermediary (CBI), is a registered financial services advisor representative and securities agent with a Series 63 license. Dave graduated with a degree in finance from the Wharton School of Business, University of Pennsylvania. For more information or a free consultation please contact Dave Kauppi at (630) 325-0123, email davekauppi@midmarkcap.com or visit our Web page http://www.midmarkcap.com